Stefan Kitzler, Friedhelm Victor, Pietro Saggese, Bernhard Haslhofer

Disentangling Decentralized Finance (DeFi)

Compositions

Open Access via institutional repository of Technische Universität Berlin

Document type

Preprint | Submitted version

(i. e. version that has been submitted to a publisher for (peer) review; also known as: Author’s Original

Manuscript (AOM), Original manuscript, Preprint)

Date of this version

Nov-2021

This version is available at

https://doi.org/10.14279/depositonce-12640

Citation details

Kitzler, Stefan; Victor, Friedhelm; Saggese, Pietro & Haslhofer, Bernhard (2021). Disentangling Decentralized

Finance (DeFi)Compositions. 1–11. http://dx.doi.org/10.14279/depositonce-12640.

Terms of use

cb This work is licensed under a Creative Commons Attribution 4.0 International license:

https://creativecommons.org/licenses/by/4.0/

Disentangling Decentralized Finance (DeFi) Compositions

Stefan Kitzler

Complexity Science Hub Vienna

Vienna, Austria

Friedhelm Victor

friedhelm.victor@tu-berlin.de

Technische Universität Berlin

Berlin, Germany

Pietro Saggese

pietro[email protected]

AIT - Austrian Institute of Technology

Vienna, Austria

Bernhard Haslhofer

AIT - Austrian Institute of Technology

Vienna, Austria

ABSTRACT

We present the first study on compositions of Decentralized Fi-

nance (DeFi) protocols, which aim to disrupt traditional finance

and offer financial services on top of the distributed ledgers, such

as the Ethereum. Starting from a ground-truth of

23

DeFi protocols

and

10,663,881

associated accounts, we study the interactions of

DeFi protocols and associated smart contracts from a macroscopic

perspective. We find that DEX and lending protocols have a high

degree centrality, that interactions among protocols primarily occur

in a strongly connected component, and that known community

detection cannot disentangle DeFi protocols. Therefore, we propose

an algorithm for extracting the building blocks and uncovering

the compositions of DeFi protocols. We apply the algorithm and

conduct an empirical analysis finding that swaps are the most fre-

quent building blocks and that DeFi aggregation protocols utilize

functions of many other DeFi protocols. Overall, our results and

methods contribute to a better understanding of a new family of

financial products and could play an essential role in assessing

systemic risks if DeFi continues to proliferate.

CCS CONCEPTS

•Applied computing →Digital cash;Electronic funds transfer.

KEYWORDS

decentralized finance, blockchain, networks

1 INTRODUCTION

Decentralized Finance (DeFi) stands for a new paradigm that aims to

disrupt established financial markets. It offers financial services in

the form of smart contracts, which are executable software programs

deployed on top of distributed ledger technologies (DLT) such as

Ethereum. Despite being a relatively recent development, we can

already observe rapid growth in DeFi protocols enabling lending

of virtual assets, exchanging them for other virtual assets without

intermediaries, or betting on future price developments in the form

of derivatives like options and futures. The term “financial lego” is

sometimes used because DeFi services can be composed into new

financial products and services.

DeFi Protocol

Contracts

Token

Contracts

1inch

BAT

Token

BAT/ETH

(UniSwap)

WETH

Token

ETH/USDT

(SushiSwap)

USDT

Token

EOA

User

Figure 1: A DeFi composition where BAT tokens are swapped

against USDT tokens through the DeFi service 1inch in a

single transaction. 1inch executes the swap sequentially

through the DeFi services UniSwap and SushiSwap, using

WETH as an intermediary token. In the transaction trace

graph, we can see the user calling the 1inch smart contract,

which in turn triggers several calls to DeFi protocol-, and

token smart contracts.

As an example of DeFi composition, consider Figure 1, which

illustrates a user interacting with the 1inch decentralized exchange

(DEX) aggregator Web service

1

. The user holds an amount of BAT

tokens and wants to swap them to USDT tokens. Using the Web

application, she creates a transaction against the 1inch contract,

which in turn triggers a sequence of two swaps on two DeFi proto-

cols within the same transaction: from BAT to WETH on UniSwap

and thereafter from WETH to USDT on SushiSwap. In this paper, we

study such single transaction DeFi interactions and the networks

that arise when combining multiple DeFi transactions.

1https://app.1inch.io

Kitzler et al.

Motivation. Within the last year, the total value of tokens held by

smart contracts underlying the DeFi protocols has reached 96 billion

USD [

9

], a growth rate that central banks increasingly perceive

as a risk (cf. [

24

]). While decentralization of finance offers many

opportunities, such as technological innovation or new governance

models, it can also undermine established forms of accountability

and erode the effectiveness of financial regulation and enforcement.

If these protocols are not understood and adopted more broadly,

they could have unforeseeable systemic effects on financial markets

and our society as a whole, as seen in the 2008 financial crisis [

16

].

Previous work (cf., [

7

,

13

]) has already shown possible strategies

allowing rational agents to maximize their revenues by subverting

the intended design of DeFi protocols. However, so far, this has

only been discussed within the restricted scope of an individual

decentralized exchange or lending protocol. Furthermore, none of

the existing studies have systematically investigated compositions

of DeFi protocols, which form complex, interconnected financial

constructs that can only be understood if we first disentangle them.

Contributions. Our work aims to analyze DeFi protocols and to

develop a novel algorithmic method that helps to understand them.

We can summarize our contributions as follows:

(1)

We provide a manually curated ground-truth of

23

DeFi

protocols and

10,663,881

associated smart contracts and

construct two network abstractions representing interac-

tions among DeFi protocols and smart contracts (Section 3).

(2)

We study intertwined DeFi protocols from a macroscopic

perspective by analyzing the topology of both networks.

We find that DEX and lending protocols have a high degree

centrality and that protocols interactions primarily occur in

a strongly connected component. We also find that known

community detection algorithms cannot disentangle DeFi

protocols, indicating DeFi compositions (Section 4).

(3)

We address the microscopic transaction level and propose

an algorithm for extracting the building blocks of DeFi pro-

tocols. We apply the algorithm to all protocol transactions

in our ground-truth, identify the most frequent building

blocks, and find swaps being the most frequent ones. We

also demonstrate how to disentangle the building blocks of

a single protocol using 1inch as an example (Section 5.1).

(4)

We present an overall picture of DeFi compositions by

extracting and flattening the entire nested building block

structure across multiple DeFi protocols. Then, we apply

our algorithm and conduct an empirical analysis showing

that DeFi aggregation protocols (1inch,0x or Instadapp)

utilize functions of many other DeFi protocols (Section 5.2).

For reproducibility of results, we make our ground-truth dataset,

including the labels as well as our source code, openly available at

https://github.com/StefanKit/Untangling_DeFi_Composition.

Implications. We believe that our results are an essential contribu-

tion towards understanding DeFi compositions. Furthermore, our

algorithm can help assess the composition of individual protocols.

Considering the volume of the global financial markets, DeFi is still

a niche phenomenon. However, if DeFi continues to proliferate and

possibly integrate with the traditional financial sector, understand-

ing DeFi compositions will be an important first step in a wider

assessment of systemic risks.

2 BACKGROUND AND DEFINITIONS

We now establish preliminary terms and definitions that are used

throughout this work and briefly introduce the related works.

2.1 Ethereum Account Types

Ethereum is currently the most important distributed ledger tech-

nology (blockchain) for DeFi services [

36

]. It differs from the Bitcoin

blockchain conceptually as it implements the so-called “account

model” with two different account types: an externally owned

account (

𝐸𝑂𝐴

) is a “regular” account controlled by a private key

held by some user. A code account (

𝐶𝐴

), which is synonymous

with the notion “smart contract”, is an account controlled by a com-

puter program, which is invoked by issuing a transaction with the

code account as the recipient.

ACA must always be initially called by an external transaction

originating from an

𝐸𝑂𝐴

, but a CA can itself trigger other CAs. In

the latter case, the interaction, which is also known as “message”, is

denoted as an internal transaction. Several branches of internal

transactions with varying depth can follow an external transaction,

resulting in a cascade, which is also called traces.

CAs allow users to implement application-layer protocols, which

are essentially programs that can follow some standardized inter-

face. Tokens are popular CA-based applications and a way to define

arbitrary assets that can be transferred between accounts. The pro-

gram behind a token manages token ownership and can implement

a standardized interface like ERC20, which defines functions stan-

dardizing token transfer semantics.

2.2 Decentralized Finance (DeFi) Protocol

ADeFi protocol is an application-layer program that provides

financial service functions such as swapping or lending assets. More

technically, we can define it as follows:

Definition 2.1. A DeFi protocol

𝑃

is a decentralized application

that facilitates specific financial service functions defined and im-

plemented by a set of protocol-specific code accounts.

The following properties distinguish DeFi services from tradi-

tional financial services: first, they are non-custodial, meaning that

no intermediary such as a bank or a broker holds custody of a users’

funds. Second, they are permissionless, meaning that anyone can

use existing or implement new services. Third, they are transparent,

which means that anyone with the necessary technical capabilities

and skills can investigate and audit the state of protocols.

2.3 DeFi Protocol Compositions

The fourth, and in this work most crucial property of DeFi protocols

is that DeFi protocols are composable:CAs can call each other, and

their individual functions can be arbitrarily composed into new

financial products and services (“Financial Lego”) [

33

]. While this

analogy is widely used in the literature, to the best of our knowl-

edge, no work investigates which are the basic composable building

blocks of more complex financial services and how they are related.

Harvey et al. [

15

] refer broadly to composability as asset tokeniza-

tion and networked liquidity, while Watcher et al. [

29

] conceive

composability narrowly as a repeated wrapping operation of to-

kens resulting in new derivative products. However, as illustrated

Disentangling Decentralized Finance (DeFi) Compositions

before in Figure 1, we note that DeFi compositions also involve CAs,

which are not tokens. Also, Engel and Herlihy [

10

] and Tolmach

et al. [

26

] respectively discuss compositions only in the context of

automated market makers (AMMs) and of formal verification of

CAs related to decentralized exchanges and lending services, which

is again a very narrow conception. Thus, there is no comprehensive,

technically grounded definition for DeFi compositions to the best

of our knowledge. For our work, we define it as follows:

Definition 2.2. A DeFi protocol composition occurs when an

account leverages one or more accounts belonging to at least an-

other DeFi protocol within a single transaction to provide a novel

financial service.

2.4 Related Work

Others studied networks closely related to the ones we investigated

before this work: Lee et al. [

18

] analyzed the local and global prop-

erties of interaction networks extracted from the entire Ethereum

blockchain statically found heavy-tailed degree distributions. In

a follow-up, Zhao et al. [

37

] analyzed the temporal evolution of

Ethereum interaction networks and found that they proliferate and

follow the preferential attachment growth model. Furthermore, sev-

eral studies focus on the network of Ethereum’s tokenized assets:

Somin et al. [

25

], for instance, studied the combined graph of all

fungible token networks, while Victor and Lüders [

28

] explored

the networks of the top 1,000 ERC20 tokens individually. Fröwis et

al. [

11

] proposed a method for detecting token systems indepen-

dent of an implementation standard. Also, Chen et al. [

5

] conducted

a systematic investigation of the whole Ethereum ERC20 token

ecosystem and analyzed their activeness, purpose, relationship, and

role in token trading. However, none of these related works consider

networks that represent DeFi Protocols and their relationships.

Another growing body of research concentrates on specific func-

tions offered by individual DeFi protocols or types of protocols.

We are aware of many DEX-related measurements focusing on

protocol-specific aspects, such as the magnitude of cyclic arbitrage

activity [

31

], the behavior of liquidity providers [

32

], or the role

of oracles as providers of external information [

19

]. Other studies

focus on lending and borrowing services: Perez et al. [

21

] analyze

liquidations and related participants’ behavior in the DeFi protocol

Compound, while Gudgeon et al. [

14

] compare market efficiency,

utilization, and borrowing rates in different lending protocols. Also,

Wang et al. [

30

] provide methods to identify flash loans in three

different DeFi providers and measure their related activity. Finally,

we are aware that von Wachter et al. [

29

] investigate composability

from an asset perspective and measure composability by identifying

the number of derivatives produced from an initial root asset. How-

ever, we apply a more technical, service-oriented perspective and

consider, to put it simply, a DeFi composition as being a computer

program utilizing other programs’ functions.

Overall, we are not aware of previous studies providing a com-

prehensive picture of DeFi compositions across various protocols.

We also do not know any work that analyzes in detail the building

blocks of individual DeFi protocols. With this work, we want to

close this gap.

3

DATASET AND NETWORK CONSTRUCTION

This section describes the data we collected and network abstrac-

tions we constructed for subsequent analysis steps.

3.1 Dataset collection

To study DeFi compositions, we are interested in transactions be-

tween Ethereum code accounts associated with known DeFi proto-

cols. Thus, we used on-chain transaction data from the Ethereum

blockchain and built a ground-truth of known CAs and their asso-

ciations to DeFi protocols.

3.1.1 On-chain transaction data. We used an OpenEthereum client

and ethereum-etl

2

to gather all Ethereum transactions from 01-Jan-

2021 (block 11,565,019) to 05-Aug-2021 (block 12,964,999), covering

the most recent DeFi history. We collected each external transaction

and also parsed its cascade of internal transactions, which together

gives us the trace. For each transaction, we extracted the source and

destination account addresses, the transaction hash, the transferred

value, the transaction type (call, create, or self-destroy), as well

as the trace id, which indexes the transactions by their execution

order. Additionally, we collected the method id of the 4-byte in-

put sequence, which allows us to identify the signature of called

methods using the 4Byte lookup service3.

To distinguish between CAs and EOA, we gathered all code ac-

count creation transactions from the first CA created on Ethereum

until the end of our observation period. We also use these cre-

ation traces to associate each CA with its creator CA. In total, we

found

46,112,390

CAs and used the output byte sequence to identify

324,143 contracts conforming to the ERC20 standard.

3.1.2 Ground-truth data. We focus on the most relevant protocols

regarding valuation and gas-burned from 06-Mar-2021 to 05-Aug-

2021. We use monthly samples of the top three total-value-locked

protocols from DeFi Pulse

4

for each financial service category to

define the set of investigated DeFi protocols. We exclude those in

the payment category because services like Polygon provide off-

chain functionality rather than composable financial services or

products. Additionally, we consider protocols including CAs of the

top ten gas burner list5in the observation period.

After identifying the most relevant DeFi protocols, we manually

collected the CAs associated with each protocol. Since this infor-

mation is not available on the blockchain, we rely on off-chain

and publicly available sources like protocol websites and available

documentation. We resolved conflicts of duplicated CA to protocol

assignments and identical names by querying CA addresses on

Etherscan

6

and uniquely assigned each CA address to its original

protocol and obtained a unique label. We denote these manually

collected data points as seed data and make them available as part

of our source code repository.

Next, we extended our seed data by implementing a heuristic

that uses the creation transactions and identifies the CAs deployed

by each seed address. By default, all extended addresses inherit

the label and protocol assignments from the corresponding seed

2https://github.com/blockchain-etl/ethereum-etl

3https://www.4byte.directory/

4https://defipulse.com/

5https://ethgasstation.info/gasguzzlers.php

6https://etherscan.io/

Kitzler et al.

Table 1: Ground-truth dataset summary statistics. Seed ad-

dresses were collected manually for each DeFi protocol and

then heuristically extended.

Number of addresses

Protocol type Seed Seed extended

Assets 289 1311

Derivatives 390 400

DEX 242 10,397,838

Lending 486 264,262

1407 10,663,811

address. Combined with our seed data, these extended addresses

form our extended seed data set. If an extended address conflicts with

an existing seed address, we keep the deployed CA and remove the

seed address. Table 1 summarizes the number of seed and extended

addresses collected for each DeFi protocol category. It shows that

our automated expansion does not increase the number of addresses

associated with DeFi protocols for assets and derivatives. However,

it massively expands the dataset for DEXs and lending protocols

utilizing automated factory contract deployments. A significant

share of the DEX addresses belongs to 1inch due to the use of gas

tokens. For more details on considered DeFi protocols, we refer to

Table 6 in the Appendix.

3.1.3 Dataset reduction. As we are only interested in known DeFi

protocols, we finally limited and reduced the traces data set to

the subset protocol traces, where the initial external transaction

originating from an EOA triggers a CA address in our extended

seed dataset. This reduction allows us to investigate and interpret

compositions within the context of known protocols.

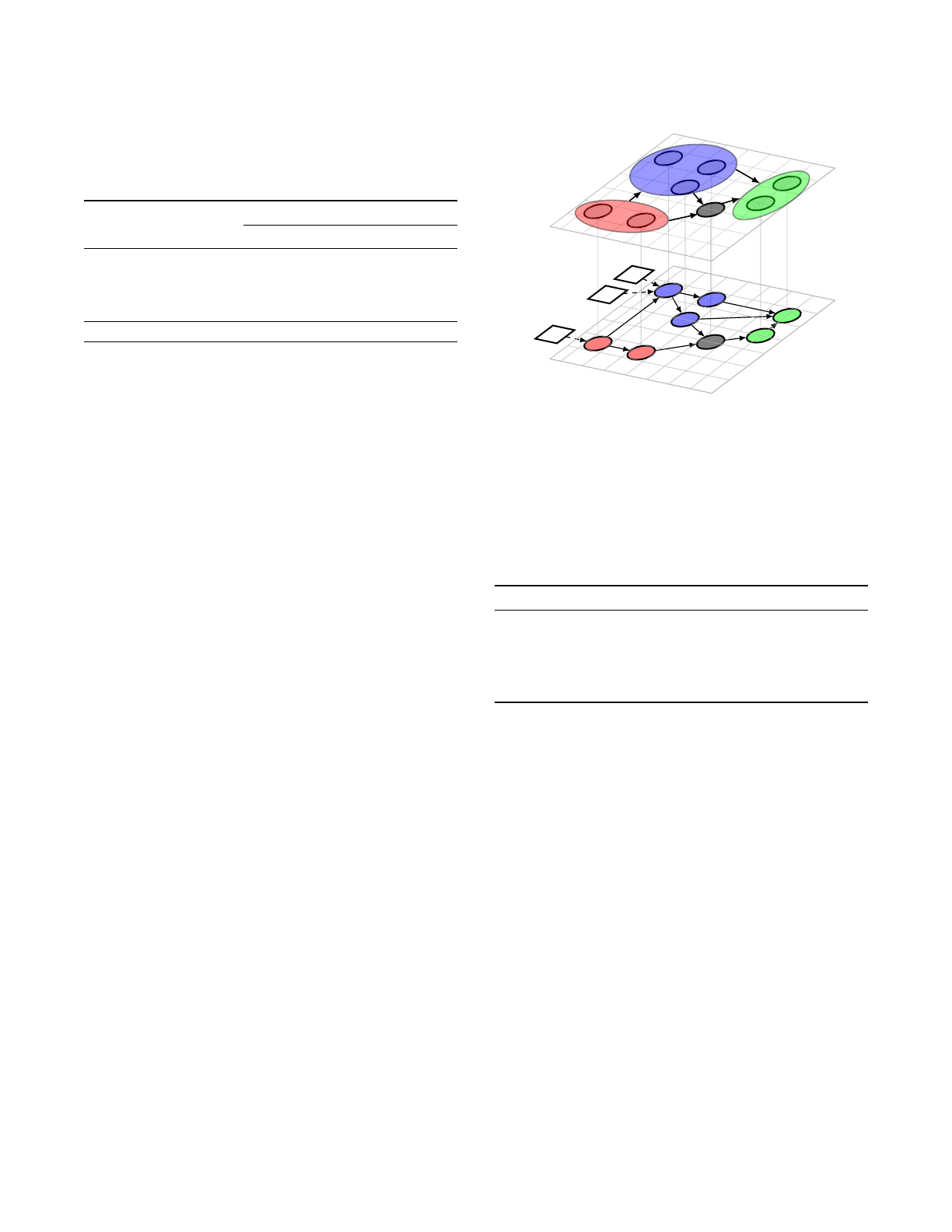

3.2 Network construction

In our analysis, we want to understand and discover relations be-

tween DeFi protocols and associated CAs. For that purpose, as

shown in Figure 2, we constructed networks consisting of DeFi

traces on two abstraction levels: the lower-level DeFi Code Account

(CA) Network network and the higher-level DeFi Protocol Network.

The DeFi CA network includes all known ground-truth CAs

triggered by external transactions from arbitrary EOA addresses and

all CAs subsequently called by cascades of internal transactions. We

note that CAs in the network can or cannot be associated with a DeFi

protocol in our ground-truth dataset. We construct the network by

filtering all internal and external transactions between CAs from

the protocol traces. Since repeated usage of DeFi services results in

recurring transaction patterns, we aggregate and count transactions

with the same source and destination address.

The DeFi Protocol network represents interactions between pro-

tocols. We constructed it by merging all DeFi CA vertices associated

with the same DeFi protocol into a single node.

We note that we modeled both networks as a directed graph,

in which vertices represent either a protocol or a single CA. The

weighted edges represent the aggregated set of transactions be-

tween DeFi protocols or CAs.

𝐶𝐴1𝐶𝐴2

𝐶𝐴3

𝐶𝐴4𝐶𝐴5

𝐶𝐴6

𝐶𝐴7

𝐶𝐴8

𝐸𝑂𝐴1

𝐸𝑂𝐴2

𝐸𝑂𝐴3

𝐶𝐴1𝐶𝐴2

𝐶𝐴3

𝐶𝐴4𝐶𝐴5

𝐶𝐴6

𝐶𝐴7

𝐶𝐴8

DeFi Protocol Network

𝑃1

𝑃2

𝑃3

DeFi CA Network

Figure 2: Schematic illustration of constructed networks. The

lower-level DeFi Code Account (CA) network represents in-

teractions between CAs. The higher-level DeFi Protocol Net-

work models relations between DeFi protocols. Lower-level

CAs vertices are associated with higher-level protocol ver-

tices. CAs are triggered by EOA or other CAs.

Table 2: Summary statistics of the analyzed networks.

DeFi CA network DeFi Protocol network

Nodes 2,536,371 43,624

Edges 3,472,757 84,789

Self-loops 6668 146

Average degree 1.369 1.944

Density 5.398e-07 4.456e-05

4 TOPOLOGY MEASUREMENTS

We now analyze the constructed networks from a macroscopic

perspective and investigate whether and how their topological

properties are affected by compositions. Table 2 reports basic sum-

mary statistics for the DeFi CA network and the DeFi Protocol

network. The main difference is in the network dimension, the

latter being two orders of magnitude smaller. The presence of self-

loops indicates that some contracts include multiple functionalities

and thus can also call themselves. Both networks are sparse, as

shown by the average degree and density measure, suggesting that

CAs tend to interact with only a few other CAs.

4.1 Degree distribution

Looking at the total-value-locked at DeFi Pulse, we can observe

that some DeFi protocols and their contracts play a major role.

This observation suggests that they implement core functionality,

which other protocols in DeFi compositions can utilize. Under this

assumption, preferential attachment [

1

,

22

] is a plausible generative

mechanism for both networks. More generally, networks whose

degree distribution follows a power law, i.e., the fraction of vertices

with degree

𝑘

is given by

𝑃(𝑘) ∼ 𝑘−𝛼

for values of

𝑘≥𝑘𝑚𝑖𝑛

, are

Loading more pages...