Vol.:(0123456789)

Review of Managerial Science

https://doi.org/10.1007/s11846-020-00429-6

1 3

ORIGINAL PAPER

Local preferences andtheallocation ofattention

inequity‑based crowdfunding

MarcoBade1· MartinWalther1

Received: 1 April 2020 / Accepted: 2 December 2020

© The Author(s) 2021

Abstract

This study examines drivers of investment probability in equity-based crowdfunding

using a hand-collected and comprehensive data set from a well-established platform.

The analysis confirms several effects that have been reported in the recent literature

on other crowdfunding markets. Extending recent research, we study moderators of

local preferences of investors. Novel to the literature, we find that (1) local pref-

erences are more pronounced in campaigns of younger ventures, (2) herding-like

behaviour is stronger in local campaigns and (3) local investors are more respon-

sive to updates posted by entrepreneurs, compared to non-locals. Our results suggest

that investors allocate more attention to campaigns for which they have information

advantages, such as local campaigns, due to their limited capacity to process infor-

mation. Such behaviour may eventually amplify information asymmetry and local

preferences. Our findings have practical implications for entrepreneurs, investors

and platforms.

Keywords Individual investor behaviour· Local preferences· Attention allocation·

Limited information processing capacity· Equity-based crowdfunding

JEL Classification D83· G11· L26· M13

1 Introduction

Recently, alternative forms of business financing, such as equity-based crowdfund-

ing, have emerged and are on the rise. In particular, the transaction value of equity-

based crowdfunding in Europe (excluding the UK) has grown from 63.1 million

* Marco Bade

Martin Walther

martin.w[email protected]

1 Chair ofFinance andInvestment, Technische Universitaet Berlin, Sec. H 64, Straße des 17. Juni

135, 10623Berlin, Germany

M.Bade, M.Walther

1 3

EUR in 2012 to 278.1 million EUR in 2018 (Statista 2020). Therefore, the topic

continuously gains attention of researchers. Equity-based crowdfunding is defined as

“[…] a form of financing in which entrepreneurs make an open call to sell a speci-

fied amount of equity or bond-like shares in a company on the Internet, hoping to

attract a large group of investors” (Ahlers etal. 2015, p. 955).

Remarkably, recent research confirms that crowdfunders tend to invest in ven-

tures which are located nearby. The overrepresentation of local assets in a portfolio

is commonly referred to as “home bias” or “local bias”.1 In the following, we refer

to “local preference” as a higher probability of investors to invest in local ventures.

Since French and Poterba (1991), a steadily growing stream of literature has dealt

with the phenomenon of home bias in many different contexts, for example, interna-

tional trade (Wolf 2000; Hillberry and Hummels 2003; Disdier and Head 2008) and

financial investment decisions (Cooper and Kaplanis 1994; Coval and Moskowitz

1999; Stuart and Sorenson 2003; Ahearne etal. 2004; Karlsson and Nordén 2007;

Graham etal. 2009; Dziuda and Mondria 2012).

In the crowdfunding context, Agrawal et al. (2015) examine the prepurchase

platform “SellaBand” that connects musicians with funders. Compared to distant

funders, local funders appear to be less responsive to information about the cumula-

tive investments in an artist. However, this distance-related effect is explained by

funders who fall into the category “friends and family”. According to Hornuf etal.

(2020), the local bias is also present on the German equity-crowdfunding platform

“Innovestment”. Likewise, in the context of equity-based crowdfunding, based on

data from the “ASSOB” equity-based crowdfunding platform, Guenther etal. (2018)

show that geographic distance is negatively correlated with investment probabil-

ity for home country investors. In contrast, overseas investors are not sensitive to

distance. By employing a quasi-experimental design, Lin and Viswanathan (2016)

investigate the mechanisms behind local bias on a virtual peer-to-peer-lending mar-

ketplace called “Prosper”. They find evidence that local bias exists in peer-to-peer

lending. They argue that economic-based explanations cannot fully explain local

bias. Instead, behavioural reasons, such as the familiarity bias, drive this phenom-

enon at least partially.

We aim to contribute to this stream of literature in two ways. First, we test

whether recent findings on drivers of investment decisions in crowdfunding can be

confirmed using a unique hand-collected data set from a well-established platform

and a modified dyadic approach based on Agrawal etal. (2015). Second and new to

the literature, we explore interactions between these drivers and geographic proxim-

ity, in order to examine the explanation of local preferences related to asymmetric

information, in particular the limited information processing capacity and attention

allocation of investors (see, e.g., Sims 2003; van Nieuwerburgh and Veldkamp 2009;

Mondria and Wu 2010).

For this purpose, we investigate several hypotheses that are expected to pro-

vide novel insights. First, we test how the degree of publicly available information

1 Note that the first relates to local preferences across borders and the second refers to local preferences

within countries.

1 3

Local preferences andtheallocation ofattention in…

(proxied by venture age) moderates local preferences. It seems natural to assume

that locals’ information advantages are particularly pronounced in younger ventures.

Therefore, investor’ preference to invest in local campaigns might be stronger the

younger the venture. In our analysis, we aim to substantiate this intuition. Second,

we examine whether locals or non-locals are more responsive to signals (posted

updates) by presumably better-informed entrepreneurs. Third, we test which type of

investor is more responsive to signals from peer investors (recent previous invest-

ments). On the one hand, it seems intuitive that signalling by entrepreneurs or by

peer investors alleviates asymmetric information between locals and non-locals and

thus reduces local preferences. On the other hand, however, if investors pay more

attention to signals concerning local campaigns, as is suggested by the attention-

allocation theory, it is conceivable that information asymmetry and local preferences

get reinforced by updates or recent previous investments. Our study aims to help

clarifying this puzzle.

The results of our study confirm the existence of local preferences in equity-based

crowdfunding. Consistent with recent research, we find indication for L-shaped

investment patterns (Hornuf and Schwienbacher 2018), herding-like behaviour (e.g.,

Hornuf and Schwienbacher 2018; Vismara 2018; Walther and Bade 2020) and a

positive effect of recent updates (Block etal. 2018). Remarkably, the more updates

have already been posted, the weaker the positive effect of updates. Novel to the

literature, we find that, first, local preferences of investors decrease in venture age.

Second, herding-like behaviour is more pronounced among local investors. Third,

compared to non-local investors, locals are more responsive to updates posted by

entrepreneurs. We link these new empirical findings to investors’ limited capacity to

process information and argue that our results are consistent with the related atten-

tion-allocation-based explanation of local preferences.

The remainder of the paper is organized as follows: Sect.2 presents the theory

on local preferences. Section3 develops our hypotheses. In Sect.4, we explain the

empirical setting and the sample construction. Section5 presents our economet-

ric model. Subsequently, in Sect.6, we present the results. Section7 discusses the

results of our analysis. Section8 concludes the paper.

2 Theory onlocal preferences

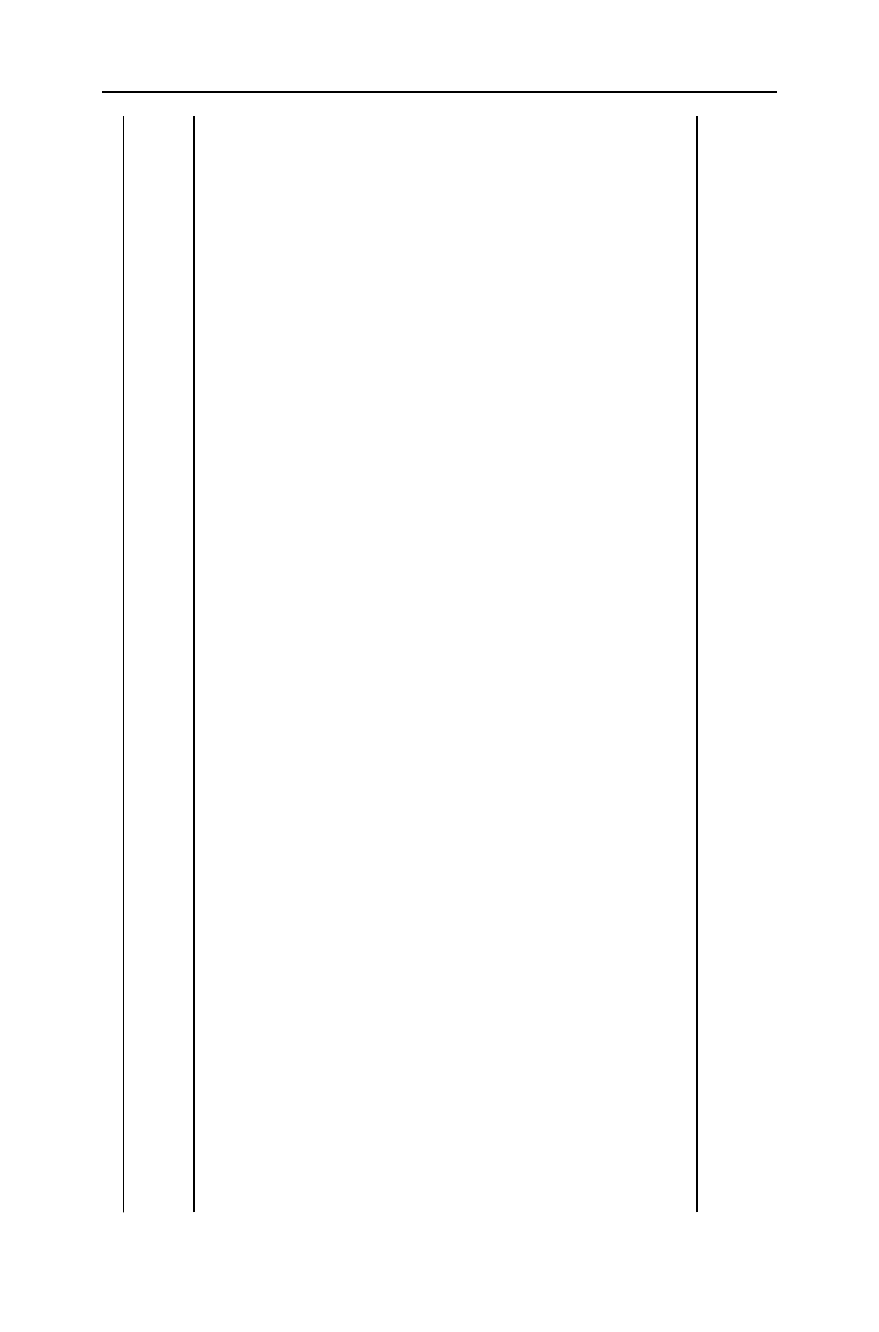

Table1 provides on overview of explanations of home bias, local bias or local pref-

erences in the non-crowdfunding-related literature. The table is structured as fol-

lows: rows represent reasons that may explain the phenomenon. The first column

lists exemplary studies focusing on the respective explanation from the non-crowd-

funding-related literature. The second column assesses the potential relevance of

each explanation for equity-based crowdfunding. The last column justifies why it

is important to investigate the respective explanation in the context of local prefer-

ences in equity-based crowdfunding. In the following subsections, we present the

theoretical background of our study based on a comprehensive literature review, in

which we refer to this table. Note that for the sake of completeness the table also

includes literature on behavioural explanations, which we do not test in this study.

M.Bade, M.Walther

1 3

Table 1 Explanations of Local Preferences

Studies in the non-crowdfunding-related

literature

Relevance for equity-based crowdfund-

ing

Why should this be investigated in the

context of local preferences in equity-

based crowdfunding?

Economic reasons (related to, e.g.,

asymmetric information and cost of

information acquisition, exchange

rates, transaction costs, riskiness of

investments)

Lewis (1999)

Coval and Moskowitz (1999)

Coval and Moskowitz (2001)

Grinblatt and Keloharju (2001)

Malloy (2005)

Ivković and Weisbenner (2005)

Kimball and Shumway (2006)

Fidora etal. (2007)

Butler (2008)

Hortaçsu etal. (2009)

Baik etal. (2010)

Most relevant: asymmetric information

- Degree of information asymmetry in

equity-based crowdfunding higher than

in other forms of crowdfunding

- Economic/financial objectives of

investors more important than in other

forms of crowdfunding

- Investors are mostly unsophisticated

and have weak skills to acquire private

information, thus might be particularly

receptive to public information signals

Transaction cost, exchange rates, etc.

more relevant in international context

and less relevant in equity-based

crowdfunding, because no product or

service is traded (no shipping cost, no

consumption of services)

Previous research in context of equity-

based crowdfunding provides mixed

evidence on the role of information

asymmetry for local preferences:

- Agrawal etal. (2015): local investors are

less responsive to public information

on cumulative investment than distants;

friends & family explain local bias

largely

- Hornuf etal. (2020): friends & family

and angel-like investors are better at

resolving information asymmetry, thus

have stronger local bias than other inves-

tor types; well-diversified investors care

less about geography

- The role of information asymmetry

between entrepreneurs and different

types of investors and within the crowd

is underexplored

- How differently informed investors

(locals vs. non-locals, non-friends-&-

family) respond to different types of

signals has not yet been studied

Idea: Investors with different levels of

information may behave differently in

terms of investments

1 3

Local preferences andtheallocation ofattention in…

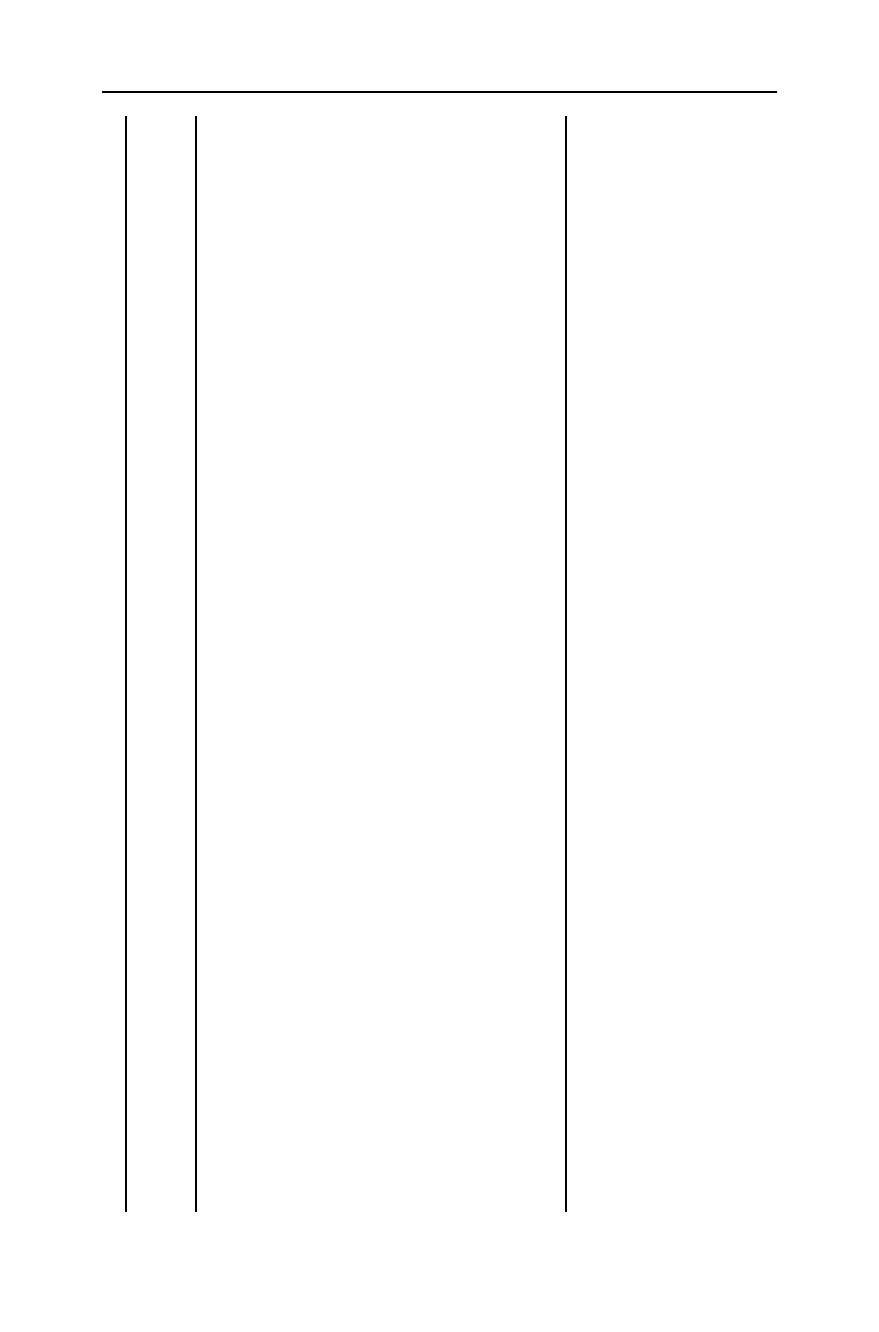

Table 1 (continued)

Studies in the non-crowdfunding-related

literature

Relevance for equity-based crowdfund-

ing

Why should this be investigated in the

context of local preferences in equity-

based crowdfunding?

Limited information processing capacity

(“Attention allocation theory”)

Van Nieuwerburgh and Veldkamp

(2009)

Mondria and Wu (2010)

Prevalence of asymmetric information,

predominance of unsophistication

among investors, weak information

processing skills, limited capital

stock suggest that investors are highly

selective concerning their allocation of

attention to campaigns in equity-based

crowdfunding

- Investors’ allocation of attention has not

yet been studied in the crowdfunding

literature

- Theory is closely connected to

information-asymmetry explanation of

local preferences

- The fact that the literature has over-

looked this theory in the context of

crowdfunding opens research gap

- Understanding how investors’ attention

allocation in the presence of asymmetric

information affects local preferences is

important for entrepreneurs, platforms

and investors themselves

Idea: Locals have superior information;

theory suggests that investors are dif-

ferently attentive to local and remote

campaigns, thus respond differently to

information signals

Loading more pages...